[ad_1]

At this time we are going to run by means of a technique of estimating the intrinsic worth of BBMG Company (HKG:2009) by taking the forecast future money flows of the corporate and discounting them again to at the moment’s worth. We are going to use the Discounted Money Stream (DCF) mannequin on this event. Do not get delay by the jargon, the mathematics behind it’s really fairly easy.

Corporations may be valued in plenty of methods, so we’d level out {that a} DCF just isn’t excellent for each state of affairs. Should you nonetheless have some burning questions on this sort of valuation, check out the Merely Wall St evaluation mannequin.

See our newest evaluation for BBMG

The mannequin

We use what is named a 2-stage mannequin, which merely means we have now two completely different durations of progress charges for the corporate’s money flows. Typically the primary stage is larger progress, and the second stage is a decrease progress section. Within the first stage we have to estimate the money flows to the enterprise over the subsequent ten years. Seeing as no analyst estimates of free money circulation can be found to us, we have now extrapolate the earlier free money circulation (FCF) from the corporate’s final reported worth. We assume corporations with shrinking free money circulation will gradual their fee of shrinkage, and that corporations with rising free money circulation will see their progress fee gradual, over this era. We do that to mirror that progress tends to gradual extra within the early years than it does in later years.

A DCF is all about the concept that a greenback sooner or later is much less useful than a greenback at the moment, and so the sum of those future money flows is then discounted to at the moment’s worth:

10-year free money circulation (FCF) forecast

| 2022 | 2023 | 2024 | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | |

| Levered FCF (CN¥, Hundreds of thousands) | CN¥3.63b | CN¥2.45b | CN¥1.91b | CN¥1.62b | CN¥1.46b | CN¥1.36b | CN¥1.30b | CN¥1.27b | CN¥1.25b | CN¥1.25b |

| Progress Charge Estimate Supply | Est @ -46.81% | Est @ -32.32% | Est @ -22.18% | Est @ -15.08% | Est @ -10.11% | Est @ -6.64% | Est @ -4.2% | Est @ -2.5% | Est @ -1.3% | Est @ -0.47% |

| Current Worth (CN¥, Hundreds of thousands) Discounted @ 11% | CN¥3.3k | CN¥2.0k | CN¥1.4k | CN¥1.1k | CN¥851 | CN¥714 | CN¥614 | CN¥537 | CN¥476 | CN¥426 |

(“Est” = FCF progress fee estimated by Merely Wall St)

Current Worth of 10-year Money Stream (PVCF) = CN¥11b

We now have to calculate the Terminal Worth, which accounts for all the longer term money flows after this ten 12 months interval. The Gordon Progress formulation is used to calculate Terminal Worth at a future annual progress fee equal to the 5-year common of the 10-year authorities bond yield of 1.5%. We low cost the terminal money flows to at the moment’s worth at a value of fairness of 11%.

Terminal Worth (TV)= FCF2031 × (1 + g) ÷ (r – g) = CN¥1.2b× (1 + 1.5%) ÷ (11%– 1.5%) = CN¥13b

Current Worth of Terminal Worth (PVTV)= TV / (1 + r)10= CN¥13b÷ ( 1 + 11%)10= CN¥4.4b

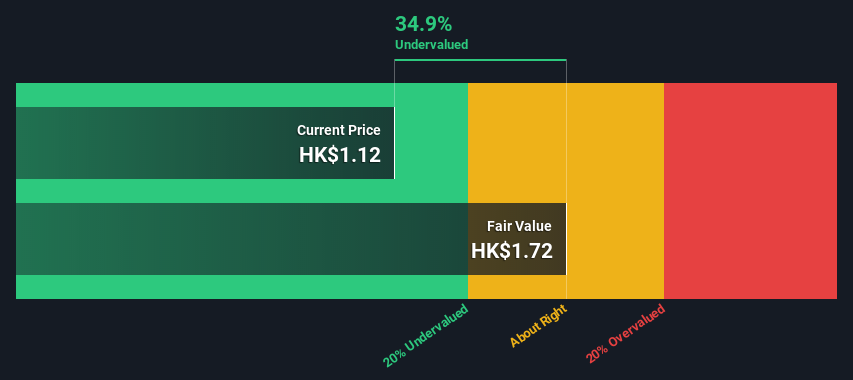

The full worth is the sum of money flows for the subsequent ten years plus the discounted terminal worth, which leads to the Whole Fairness Worth, which on this case is CN¥16b. Within the ultimate step we divide the fairness worth by the variety of shares excellent. In comparison with the present share value of HK$1.1, the corporate seems fairly good worth at a 35% low cost to the place the inventory value trades presently. Bear in mind although, that that is simply an approximate valuation, and like all advanced formulation – rubbish in, rubbish out.

Necessary assumptions

We might level out that crucial inputs to a reduced money circulation are the low cost fee and naturally the precise money flows. Should you do not agree with these consequence, have a go on the calculation your self and play with the assumptions. The DCF additionally doesn’t contemplate the potential cyclicality of an trade, or an organization’s future capital necessities, so it doesn’t give a full image of an organization’s potential efficiency. Provided that we’re taking a look at BBMG as potential shareholders, the price of fairness is used because the low cost fee, somewhat than the price of capital (or weighted common value of capital, WACC) which accounts for debt. On this calculation we have used 11%, which is predicated on a levered beta of two.000. Beta is a measure of a inventory’s volatility, in comparison with the market as an entire. We get our beta from the trade common beta of worldwide comparable corporations, with an imposed restrict between 0.8 and a pair of.0, which is an inexpensive vary for a steady enterprise.

Subsequent Steps:

Valuation is just one aspect of the coin when it comes to constructing your funding thesis, and it should not be the one metric you have a look at when researching an organization. It is not potential to acquire a foolproof valuation with a DCF mannequin. Slightly it needs to be seen as a information to “what assumptions should be true for this inventory to be underneath/overvalued?” For instance, modifications within the firm’s value of fairness or the danger free fee can considerably influence the valuation. What’s the cause for the share value sitting beneath the intrinsic worth? For BBMG, there are three related elements you need to additional look at:

- Dangers: Take dangers, for instance – BBMG has 4 warning indicators (and a pair of that are doubtlessly severe) we predict you need to find out about.

- Future Earnings: How does 2009’s progress fee evaluate to its friends and the broader market? Dig deeper into the analyst consensus quantity for the upcoming years by interacting with our free analyst progress expectation chart.

- Different Strong Companies: Low debt, excessive returns on fairness and good previous efficiency are basic to a powerful enterprise. Why not discover our interactive record of shares with strong enterprise fundamentals to see if there are different corporations you might not have thought-about!

PS. Merely Wall St updates its DCF calculation for each Hong Kong inventory day-after-day, so if you wish to discover the intrinsic worth of some other inventory simply search right here.

Have suggestions on this text? Involved in regards to the content material? Get in contact with us immediately. Alternatively, electronic mail editorial-team (at) simplywallst.com.

This text by Merely Wall St is basic in nature. We offer commentary primarily based on historic knowledge and analyst forecasts solely utilizing an unbiased methodology and our articles aren’t meant to be monetary recommendation. It doesn’t represent a advice to purchase or promote any inventory, and doesn’t take account of your goals, or your monetary state of affairs. We goal to deliver you long-term centered evaluation pushed by basic knowledge. Be aware that our evaluation might not issue within the newest price-sensitive firm bulletins or qualitative materials. Merely Wall St has no place in any shares talked about.

[ad_2]

Source link

/cloudfront-us-east-2.images.arcpublishing.com/reuters/54CZWTH7OBI4XCIIPFKA2JZUQM.jpg)

/cloudfront-us-east-2.images.arcpublishing.com/reuters/UE6M4QUVOZPYLBRQXSROQVGVEE.jpg)