[ad_1]

Nattakorn Maneerat/iStock by way of Getty Pictures

Plenty of issues occurred final week, and it has been a problem to try to join the transferring components. Shares are on observe to register their sixth straight week of declines for the primary time for the reason that confluence of the eurozone monetary disaster, credit standing downgrade of US Treasuries and a debt disaster debacle in Congress despatched equities reeling within the late summer season of 2011. The cryptocurrency market seems to be in meltdown mode. And nominal junk bond yields have virtually caught up with inflation (not fairly, although, because the ICE BofA Excessive Yield index is at 7.4 % and headline CPI weighs in at 8.3 %). The struggle in Ukraine slogs on, Shanghai continues to be caught in lockdown and Fed watchers stay obsessively glued to each utterance from an Open Market Committee voting member who would possibly drop trace of a 0.75 % transfer subsequent time (in useless, as a result of the Fed actually does appear to have circled the wagons round 0.5 %).

The Clubber Lang Idea of Markets

The strand that weaves via all these transferring components is a reality of market life referred to as the ache commerce. Within the film Rocky III, the heavyweight challenger Clubber Lang, performed to perfection by Mr. T, is requested what he predicts will occur within the upcoming battle in opposition to Stallone’s Rocky Balboa. “My prediction? My prediction is… ache!” snarls the fearsome Lang.

For traders who take the benefit of margin leverage to pile into scorching markets, ache considerably akin to a nasty left hook from Clubber Lang occurs when their positions go far south and they should give you liquid funds to cowl margin calls. Promoting begets extra promoting. When the S&P 500 fell beneath 4,000 earlier final week, quite a few market analysts noticed that as a ache threshold more likely to unleash extra near-term promoting associated to margin calls.

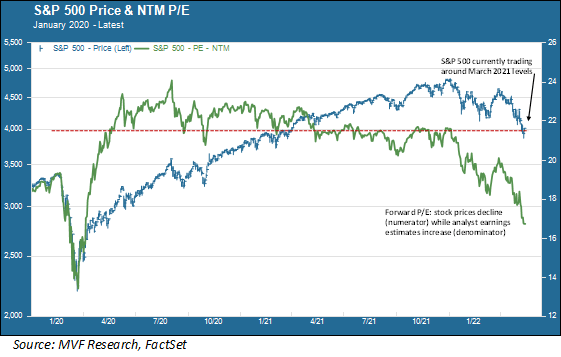

S&P 500 Worth And NTM P/E (Writer)

Trying on the above chart, it’s not instantly clear why 4,000 ought to be a ache commerce threshold, aside from that it’s a good spherical quantity and form of bifurcates the lengthy rally in shares that began when the Fed stepped into the pandemic disaster in late March 2020. You may have a look at that crimson dotted line on the chart connecting present inventory costs to their ranges in March ’21 and see that anybody who leveraged up someplace between then and now can be feeling various levels of ache.

Stablecoins and Different Magical Issues

After all, traders loaded up on far more than the blue-chip shares on the S&P 500 through the good instances. Now, many a prediction has been made many a time concerning the imminent demise of cryptocurrencies as they implausibly zoomed via the stratosphere during the last couple years. A pair issues occurred final week, although, to recommend that this asset class could also be in for one thing greater than a passing tempest this time round. Early within the week TerraUSD (UST-USD), a so-called stablecoin, turned unmoored from its notional peg and began buying and selling at ranges typical of distressed debt – 25 or 30 cents on the greenback. The subsequent day, the most important of the stablecoin breed, Tether (USDT-USD), plummeted 5 % or so beneath the peg that’s imagined to again every greenback of the token with a greenback’s price of extremely liquid money equivalents.

Stablecoins are imagined to be a form of gateway between the worlds of conventional monetary merchandise and the wild world of purely digital belongings – cryptocurrencies like bitcoin and its ilk. For Tether to fall beneath its dollar-for-dollar peg is roughly analogous to a standard cash market fund “breaking the buck,” one thing final seen through the 2008 monetary disaster. Monetary regulators, central bankers and others who carefully observe the market have lengthy warned that stablecoins are nothing just like the absolutely backed belongings they declare to be. Unsurprisingly, then, the tremors from Terra and Tether final week have been felt far and huge all through cryptoland.

The crypto meltdown, then, feeds into the ache commerce for a similar causes that extremely leveraged positions in, say, the high-flying tech shares of latest reminiscence do. The excellent news is that there’s more likely to be nothing near the form of systemic danger that characterised the broader meltdown of the complete monetary system in 2008. Again then, all the main gamers have been caught up within the extremely leveraged asset-backed securities that originally introduced down Lehman Brothers. At this time, many giant monetary establishments do have publicity to crypto, to make sure, however for essentially the most half, it’s extra akin to toes dipped within the water than widespread systematic publicity. Unhealthy for anybody who took a serious punt on bitcoin at $60,000, not so dangerous for the so-called SIFIs, the systemically vital monetary establishments. So far as anybody is aware of, anyway.

Again To What Issues

So, what does all of this imply for conventional portfolios of shares and bonds? Circumstances stay fairly risky, with a number of value swings of 1 % or extra all through the day on many buying and selling days. Credit score danger spreads have began to widen – though, as noticed earlier on this commentary, yields on excessive yield debt are nonetheless trailing current ranges of headline inflation. Relying on how the stablecoin troubles play out, there could possibly be loads extra harm in retailer for digital belongings.

We want to level out one function of the above chart, although, to recommend that amid all of the tumult there are some good causes to maintain a transparent head concerning the underlying power of the financial system. Within the chart, we present the ahead 12-months price-to-earnings (P/E) ratio, the inexperienced line. As you may see, the ahead P/E has fallen quick over the previous 4 months. A part of this, in fact, is as a result of the inventory costs – the numerator within the P/E ratio – have come down. However on the similar time, analysts’ ahead earnings estimates for these firms – the denominator of the ratio – have really gone up, thus bringing the P/E even decrease than it could be simply from the inventory value declines.

If the analysts’ consensus is right (and we should always word that such just isn’t at all times the case), then in some unspecified time in the future an organization with a battered inventory value and a powerful progress outlook turns into a shopping for alternative. That chance will not be in the present day – like we mentioned, there could also be extra ache trades to return, and intraday markets are too frothy for implementing a rational buying and selling technique. Nevertheless it’s the longer term money flows that matter for a inventory’s long-term return prospects. If these money flows may be gotten at oversold ranges, that makes it even higher.

Unique Put up

Editor’s Be aware: The abstract bullets for this text have been chosen by Searching for Alpha editors.

[ad_2]

Source link

/cloudfront-us-east-2.images.arcpublishing.com/reuters/54CZWTH7OBI4XCIIPFKA2JZUQM.jpg)

/cloudfront-us-east-2.images.arcpublishing.com/reuters/UE6M4QUVOZPYLBRQXSROQVGVEE.jpg)

{kind=link}