[ad_1]

Richard Drury/DigitalVision through Getty Photos

In September of 2017, I acquired barely over $100K from my former employer which represented the commuted worth of my pension plan. I made a decision to take a position 100% of this cash in dividend progress shares.

Every month, I publish my outcomes on these investments. I don’t do that to brag. I do that to point out my readers that it’s potential to construct a long-lasting portfolio throughout all types of market situations. Some months we would seem to underperform, however you need to belief the method over the long run to guage our efficiency extra precisely.

Efficiency In Evaluate

Let’s begin with the numbers as of April 4th, 2022 (earlier than the bell):

Unique quantity invested in September 2017 (no extra capital added): $108,760.02.

- Portfolio worth: $219,612.22

- Dividends paid: $4,054.81 (“TTM”)

- Common yield: 1.85%

- 2021 efficiency: +16.78%

- SPY= 28.75%, XIU.TO = 28.05%

- Dividend progress: +3.14%

Complete return since inception (Sep 2017- March 2022): 102%

Annualized return (since September 2017 – 54 months): 16.91%

SPDR® S&P 500 ETF Belief (SPY) annualized return (since Sept 2017): 16.47% (whole return 98.56%)

iShares S&P/TSX 60 ETF (XIU.TO) annualized return (since Sept 2017): 12.65% (whole return 70.90%)

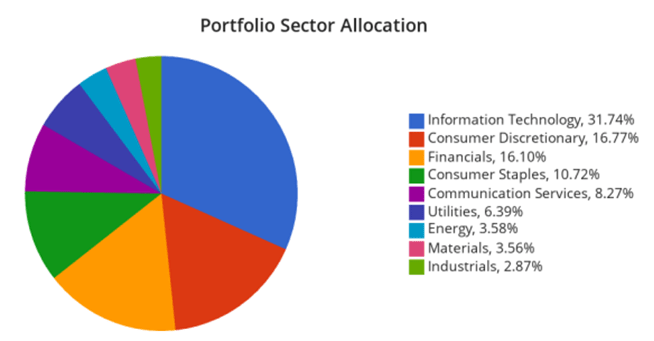

Sector allocation calculated by DSR PRO

Extra Trades

You in all probability noticed this coming from my earlier portfolio replace. I’m about to make some trades! I’m not the kind of investor who will readily bounce from one inventory to a different. In actual fact, it’s fairly the other. I spend a number of hours of high quality time analyzing corporations earlier than I make an funding choice.

Sadly, time modifications, the enterprise setting evolves, and corporations take completely different turns. In different phrases, irrespective of how a lot time you place into your evaluation, your funding thesis might flip fallacious. That is just about the story of one among my shares.

Adios Andrew!

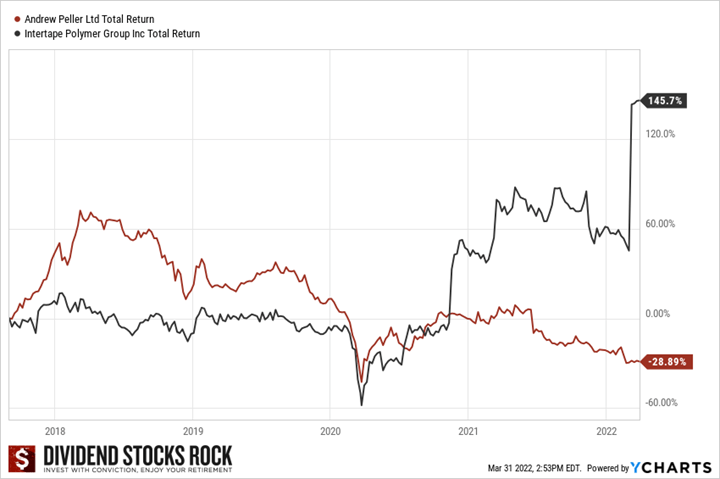

Final month, I made a decision I had sufficient of Andrew Peller’s (OTCPK:ADWPF) weak progress. One of many explanation why I purchased shares on this firm in 2017 was its progress by acquisition technique. Andrew Peller is a dominant participant within the wine trade, and it enjoys economies of scale and might promote its merchandise via its personal distribution community. Since ADWPF operates in a fragmented market, shopping for extra vineyards to help progress is a great enterprise mannequin. Sadly, they put the break on this technique in 2019 and by no means went again to it (perhaps because of the pandemic). The end result for my portfolio was horrible. After surging greater than 60% in 2018, the inventory began to say no shortly after and by no means stopped the bleeding. I bought at a lack of ~28% together with dividends! Firstly of March, I bought my 586 shares at $7.237/per share.

However I made my peace with it, and I’ve chosen to put money into a thriving enterprise going ahead!

Adios Duct Tape?

Talking of thriving companies, the acquisition of Intertape Polymer (OTCPK:ITPOF) greater than compensated for the losses incurred with my Andrew Peller shares. Intertape Polymer’s inventory surged on a giant announcement on March eighth: it is going to be acquired at $40.50 per share!

For the reason that inventory went up above $39 and the transaction is anticipated to shut in Q3, I didn’t wait lengthy and determined to take the cash and run. Shares have been buying and selling round $39.50 because the announcement, leaving a 2.5% upside potential (plus dividend) till the transaction closes. A day or two after the announcement, I bought my 128 shares at $39.20 for a ~140% whole return.

Typically you win… generally you lose…

Welcome Granite!

When you have been a follower for some time, this transaction is not going to shock you. I’ve typically talked about Granite REIT (GRP.U) being my favourite REIT. For some purpose, I by no means obtained an opportunity so as to add it to my portfolio (nice alternatives are sometimes infinite whereas my funding pockets is finite!). I purchased 128 shares at $91.70.

GRT was once an extension of Magna Worldwide (MGA). In 2011, Magna represented about 98% of its revenues. It’s now all the way down to 29% as at December 2021 (with Amazon as its second-largest tenant with 5% of income). Administration has remodeled this industrial REIT right into a well-diversified enterprise with out adversely affecting shareholders. GRT now manages 122 properties throughout 7 nations. The REIT additionally boasts an funding grade ranking of BBB/BAA2 steady. With a low FFO payout ratio (round 72%), shareholders can take pleasure in a 3%+ yield that ought to develop and match or beat the inflation fee. That is among the many uncommon REITs exhibiting AFFO per unit progress whereas issuing extra items to finance progress. Let’s simply say that Granite’s profile is loads stronger than Andrew Peller’s.

Extra Renewable Vitality!

With the remaining money within the account, I fueled my portfolio with extra renewable power (pun supposed). Firstly of March, I purchased 99 shares of Brookfield Renewable Vitality (BEPC) at $48.42. I already had a couple of shares of BEPC in my portfolio as I beforehand used dividend funds from different corporations to begin a place on this firm.

What I imply by “beginning a place” is that I choose to have equally-weighted positions in my portfolio. Subsequently, since I’ve 21 completely different corporations in my portfolio, the purpose is to have 4-5% weight in every of them. Since a few of my shares have surged because the creation of my portfolio in 2017 (good day Apple, Microsoft, Visa, and BlackRock!), my cash isn’t unfold equally throughout all my holdings. I’m utilizing dividend funds to rebalance some positions right here and there. I normally don’t do “half place” trades as I did with BEPC, however I actually wished to get in that inventory and since I can’t add capital to this account (it’s a locked-in retirement account), I needed to begin with money generated by the portfolio.

The way forward for power shall be present in hydroelectric, photo voltaic, and wind energy. 64% of BEPC’s portfolio is concentrated on hydroelectric energy. The corporate has energy vegetation in North America, South America, Europe, and Asia. BEPC enjoys large-scale capital sources and the experience to handle its tasks the world over. Administration goals at a 5-9% annual distribution improve. What is going to occur within the coming years is more cash shall be going towards these tasks. Traders are following the inexperienced pattern and BEP is well-positioned to draw them.

After this transaction, BEPC is now 3.50% of my portfolio. It’s nonetheless a small participant and I’ll seemingly proceed to extend my place with future dividend funds. There’s nothing higher than boosting your publicity to such a robust dividend grower!

Extra thought: Alimentation Couche-Tard (OTCPK:ANCUF) doesn’t get the like it deserves

Throughout my newest portfolio replace, most of my Canadian shares reported their earnings, however Couche-Tard was late to the social gathering. Whereas ANCUF is buying and selling at an all-time excessive, I proceed to consider it doesn’t get the like it deserves from the market. The inventory is buying and selling at a P/E under 19 and its newest quarterly earnings confirmed EPS up 27% and income up 6%. The rise was primarily pushed by same-store merchandise gross sales which elevated by 3.7% within the U.S., 7.2% in Europe and different areas. Identical-store gross sales dropped 0.8% in Canada. Driving greater revenues was the upper common street transportation gasoline promoting worth and demand. Merchandise and repair gross margins elevated 1% within the U.S. to 33.6%, 0.2% in Canada to 31.6%, and decreased 0.7% in Europe and different areas to 37.8%, which was impacted by the combination of Circle Ok Hong Kong.

Let’s take a look at my CDN portfolio. Numbers are as of March 4th, 2022 (after the market shut):

Canadian Portfolio (CAD)

| Firm Title | Ticker | Market Worth |

| Algonquin Energy & Utilities | AQN | 6,620.67 |

| Alimentation Couche-Tard | OTCPK:ANCUF | 20,269.14 |

| Nationwide Financial institution | OTCPK:NTIOF | 11,631.73 |

| Royal Financial institution | RY | 8,293.80 |

| Brookfield Renewable | BEPC | 7,542.09 |

| CAE | CAE | 6,856.00 |

| Enbridge | ENB | 9,378.25 |

| Fortis | FTS | 6,225.12 |

| Magna Worldwide | MGA | 5,639.90 |

| Sylogist | OTCPK:SYZLF | 3,982.35 |

| Granite REIT | GRP.U | 11,976.96 |

| Money | 139.45 | |

| Complete | $98,555.46 |

My account reveals a variation of +$9,802.07 (+11%) because the final revenue report on March 3rd. In my earlier version, I mentioned how market corrections shouldn’t impression your notion of your portfolio. As soon as once more, time labored in my favor and the general portfolio is getting near its all-time excessive. It doesn’t imply it may possibly’t go down sooner or later, however I might moderately let it work and pay dividends.

Right here’s my US portfolio now. Numbers are as March 4th, 2022 (after the market shut):

U.S. Portfolio (USD)

| Firm Title | Ticker | Market Worth |

| Activision Blizzard | ATVI | 9,364.68 |

| Apple | AAPL | 13,383.00 |

| BlackRock | BLK | 10,951.22 |

| Disney | DIS | 6,236.10 |

| Gentex | GNTX | 6,822.05 |

| Microsoft | MSFT | 17,323.35 |

| Starbucks | SBUX | 7,487.65 |

| Texas Devices | TXN | 9,135.50 |

| V.F. Company | VFC | 4,611.33 |

| Visa | V | 11,387.00 |

| Money | 306.50 | |

| Complete | $97,008.38 |

The US whole worth account reveals a variation of +$3,619.77 (+3.88%) because the final revenue report on March 3rd. Like what occurred to my Canadian portfolio, the U.S. portfolio went again up properly over the previous 2-3 weeks. There haven’t been any modifications for this portion of the portfolio.

My Complete Portfolio Up to date for Q1 2022

Every quarter, we run an unique report for Dividend Shares Rock (“DSR”) members who subscribe to our very particular extra service known as DSR PRO. The PRO report features a abstract of every firm’s earnings report for the interval. We now have been doing this for a whole yr now and I wished to share my very own DSR PRO report for this portfolio. You may obtain the complete PDF exhibiting all of the details about all my holdings. Outcomes have been up to date as of March 2022.

Obtain my portfolio Q1 2022 report.

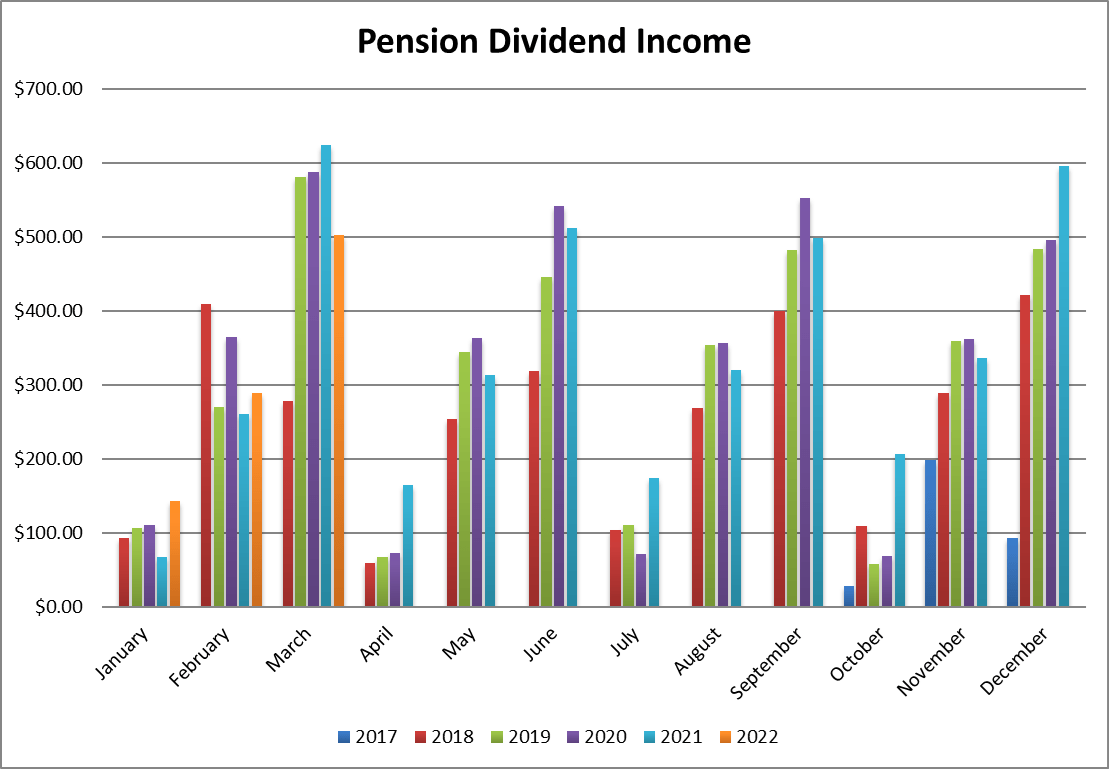

Dividend Revenue: $501.92 CAD (-19.5% vs. March 2021)

That is what occurs whenever you commerce in your portfolio! My dividend revenue took a extreme hit this quarter as a result of final yr, I acquired funds from Lazard and Intertape Polymer. I might have acquired a bigger quantity from Microsoft, however I additionally bought some shares to rebalance my portfolio in December. Lastly, I took a 1.5% forex hit because the USD/CAD conversion fee was 1.2624.

In addition to Sylogist, all my different holdings present a dividend improve vs final yr.

Right here is the element of my dividend funds.

Dividend progress (over the previous 12 months):

- Fortis: +6%

- Enbridge: +3%

- Magna Worldwide: +6.1%

- Sylogist: 0%

- Brookfield Renewable: new dividend

- Visa: +17%

- Microsoft: +1.5% (I bought some shares)

- V.F. Corp.: +2%

- BlackRock: +18%

- Forex issue: -1.5%

Canadian Holding payouts: $283.10 CAD

- Fortis: $52.97

- Enbridge: $138.46

- Magna Worldwide: $39.54

- Sylogist: $52.13

- Brookfield Renewable $17.07

U.S. Holding payouts: $161.67 USD

- Visa: $18.75

- Microsoft: $34.10

- V.F. Corp.: $40.50

- BlackRock: $68.32

Complete payouts: $484.85 CAD

*I used a USD/CAD conversion fee of 1.2479

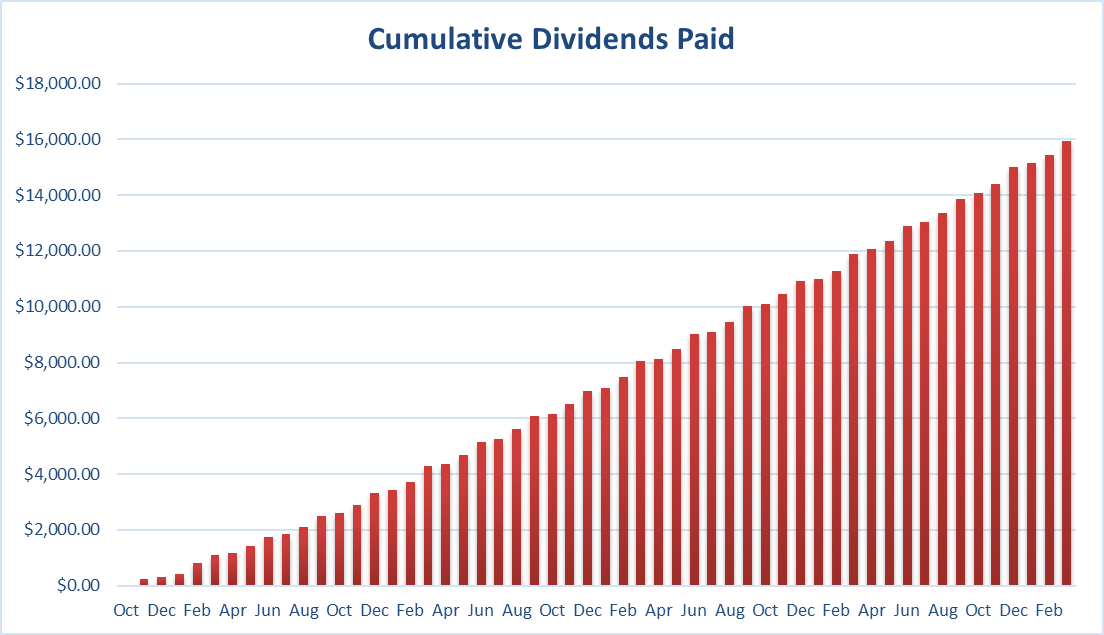

Since I began this portfolio in September 2017, I’ve acquired a complete of $15,944.01 CAD in dividends. Remember the fact that this can be a “pure dividend progress portfolio” as no capital may be added into this account apart from retained and/or reinvested dividends. Subsequently, all dividend progress is coming from the shares and never from any extra capital being added to the account.

Ultimate Ideas

Massive replace on a private degree. Since I turned 40 about six months in the past, I began to have extra ideas about constructing belongings at a quicker tempo for the subsequent decade. My monetary plan is properly on its method, however I like a problem and see wealth creation as a worthwhile passion.

Subsequently, I’ll begin a Smith Manoeuvre portfolio in April. The Smith Manoeuvre has been popularized by a financier named Fraser Smith who discovered a method via leverage to make Canadians’ mortgage curiosity tax-deductible. Leverage isn’t for everybody, however I’ll share my plan to put money into dividend progress shares through the use of a house fairness line of credit score.

Unique Submit

Editor’s Observe: The abstract bullets for this text had been chosen by In search of Alpha editors.

[ad_2]

Source link

/cloudfront-us-east-2.images.arcpublishing.com/reuters/54CZWTH7OBI4XCIIPFKA2JZUQM.jpg)

/cloudfront-us-east-2.images.arcpublishing.com/reuters/UE6M4QUVOZPYLBRQXSROQVGVEE.jpg)

{kind=link}