[ad_1]

KanawatTH/iStock through Getty Photos

At any time when motorists pump gasoline today, they get a painful reminder of Russia’s position in world oil markets. What’s been much less appreciated is the vary of uncooked and semi-finished merchandise that Russia and Ukraine export. From palladium to wheat, disruptions are already placing upward strain on costs throughout a variety of on a regular basis merchandise, heightening macroeconomic and market dangers over the approaching quarters.

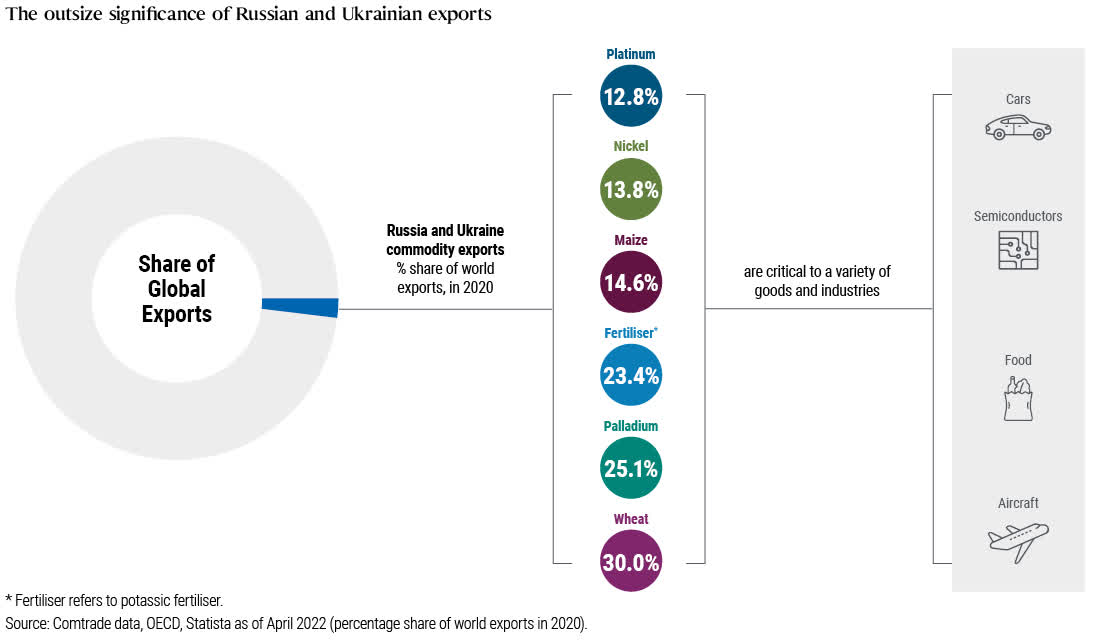

At first look, Russia and Ukraine should not matter that a lot to world financial exercise. Ukraine’s share of world exports is simply 0.3%, whereas Russia’s is 1.9%. In distinction, China and the U.S. every make up roughly 10% of world commerce.

But it is a dramatically completely different story in the case of key industrial inputs. Because the graph reveals, Ukraine and Russia are main exporters of palladium, nickel, grains, and different sources which are essential to a wide range of items and industries – from vehicles to semiconductors to groceries.

Creator

Palladium

Think about palladium, a chemical factor and uncommon valuable metallic with a silver-white look. Russia produces greater than a 3rd of the world’s palladium, a lot of it for export. Along with jewellery and dentistry, palladium is used to make catalytic converters that cut back air pollution in exhaust from inner combustion engines. They’re necessary in lots of international locations. So vehicle manufacturing – already slowed by pandemic- and supply-chain-related shortages of semiconductors – faces additional disruption.

Palladium is only one instance. Different key manufacturing inputs embody fertilizer for agriculture, neon gasoline for semiconductors, nickel for metal, and ammonia for plastics.

Market impacts

Commodity markets have been fast to cost within the provide/demand imbalances, however we imagine economists and fairness traders are behind the curve in assessing the impacts on development and company earnings.

Shortages of main inputs will probably be felt on each the demand and provide aspect of the equation. This runs the chance of snowballing and nonlinear damaging impacts on broader financial development whereas pushing inflation greater.

Second-order results are already sprouting as greater enter prices push costs greater, in some circumstances resulting in demand destruction. In latest weeks, Europe has been hit by decreased or suspended manufacturing in choose metal, fertilizer, and paper manufacturing services. The auto sector, already reeling from the semiconductor shortages of the previous 18 months, has slowed manufacturing, main trade specialists to foretell extra delays and disruptions within the coming months.

Whereas interlinkages and pass-through results are complicated and onerous to quantify, greater costs and demand destruction will sluggish development and put upward strain on costs – giving central banks an incentive to tighten coverage quicker than would in any other case have been the case.

Naturally, Europe will seemingly be hit hardest because of its proximity and financial ties to the combatants. Nonetheless, the interconnectedness of the worldwide financial system signifies that ripples will unfold, from meals costs in Egypt to costs of kids’s toys within the U.S.

Importantly, as outlined in our Cyclical Outlook, “Anti-Goldilocks,” the disruptions come amid elevated financial uncertainty with excessive inflation, slowing development, and tightening monetary situations, resulting in a fragile and precarious market atmosphere over the approaching quarters.

Funding implications

For multi-asset portfolios, we imagine this necessitates a extra defensive stance and a concentrate on high quality and liquidity, as the chance of recession rises over the cyclical horizon. Buyers might need to keep away from extra cyclical sectors inside equities, particularly in Europe the place the financial cycle seems to be most susceptible within the close to time period, in our view.

As a substitute, we favor high-quality securities with pricing energy and sturdy earnings development, in areas equivalent to semiconductor manufacturing and healthcare. We additionally like firms that may ship sustainable upside potential in a slower-growth world, in areas equivalent to renewable vitality and automation.

On the asset allocation degree, our technique has been to broaden potential return drivers into rate of interest and forex markets the place we see the higher worth, equivalent to an rising market international change. We purpose to maintain general directionality low whereas being dynamic in our danger administration.

As at all times, volatility presents each danger and alternative.

Disclosures

Previous efficiency just isn’t a assure or a dependable indicator of future outcomes.

All investments include danger and will lose worth. Investing within the bond market is topic to dangers, together with market, rate of interest, issuer, credit score, inflation danger, and liquidity danger. The worth of most bonds and bond methods are impacted by modifications in rates of interest. Bonds and bond methods with longer durations are typically extra delicate and unstable than these with shorter durations; bond costs usually fall as rates of interest rise, and low rate of interest environments enhance this danger. Reductions in bond counterparty capability might contribute to decreased market liquidity and elevated worth volatility. Bond investments could also be price kind of than the unique price when redeemed. Equities might decline in worth because of each actual and perceived normal market, financial and trade situations. Investing in foreign-denominated and/or -domiciled securities rising markets. Commodities include heightened danger, together with market, political, regulatory and pure situations, and might not be applicable for all traders. Forex charges might fluctuate considerably over quick durations of time and will cut back the returns of a portfolio. Focus of belongings in a single or a couple of international locations (or a specific space) and currencies will topic a portfolio to higher danger than if the belongings weren’t geographically concentrated. Diversification doesn’t guarantee towards loss.

Statements regarding monetary market developments or portfolio methods are primarily based on present market situations, which is able to fluctuate. There isn’t a assure that these funding methods will work beneath all market situations or are applicable for all traders and every investor ought to consider their skill to speculate long-term, particularly during times of downturn available in the market. Buyers ought to seek the advice of their funding skilled previous to investing resolution. Outlook and methods are topic to alter with out discover.

Forecasts, estimates and sure data contained herein are primarily based upon proprietary analysis and shouldn’t be thought of as funding recommendation or a advice of any specific safety, technique or funding product. There isn’t a assure that outcomes will probably be achieved.

PIMCO as a normal matter supplies companies to certified establishments, monetary intermediaries and institutional traders. Particular person traders ought to contact their very own monetary skilled to find out essentially the most applicable funding choices for his or her monetary state of affairs. This materials accommodates the opinions of the supervisor and such opinions are topic to alter with out discover. This materials has been distributed for informational functions solely and shouldn’t be thought of as funding recommendation or a advice of any specific safety, technique or funding product. It isn’t doable to speculate immediately in an unmanaged index. Info contained herein has been obtained from sources believed to be dependable, however not assured. No a part of this materials could also be reproduced in any type, or referred to in some other publication, with out specific written permission. PIMCO is a trademark of Allianz Asset Administration of America L.P. in the US and all through the world. ©2022, PIMCO.

Unique Submit

Editor’s Be aware: The abstract bullets for this text have been chosen by In search of Alpha editors.

[ad_2]

Source link

/cloudfront-us-east-2.images.arcpublishing.com/reuters/54CZWTH7OBI4XCIIPFKA2JZUQM.jpg)

/cloudfront-us-east-2.images.arcpublishing.com/reuters/UE6M4QUVOZPYLBRQXSROQVGVEE.jpg)

{kind=link}